AppLovin is an AI-powered advertising technology platform whose mission is to create meaningful connections between companies and their ideal customers.

Founded in 2011, the company was historically organized around two segments — Advertising and Apps — but completed a major strategic pivot on June 30, 2025, when it divested its entire Apps business (a portfolio of free-to-play mobile games) to Tripledot Studios for $400M in cash plus ~20% equity in Tripledot. Since that divestiture, AppLovin operates as a pure-play advertising technology company and single reportable segment.

The Business

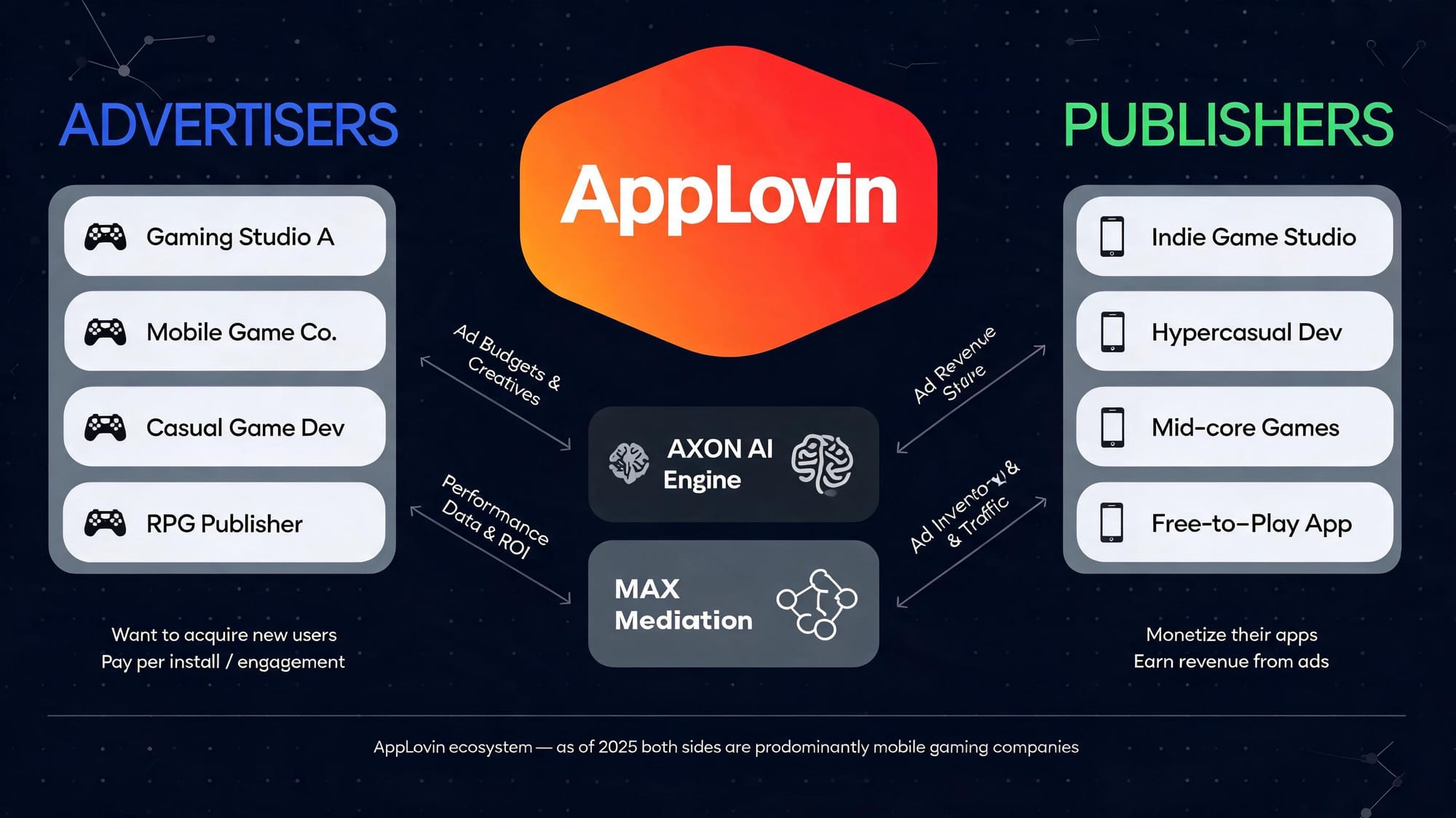

AppLovin one and only product (but made up of different tools) is an AI-powered performance-based ad marketplace used in online gaming advertising.

AppLovin acts as an agent/intermediary in the advertising ecosystem: it matches advertiser demand (historically predominantly gaming companies promoting their own mobile games) with publisher supply (ad slots in mobile games) through real-time auctions at “vast scale and microsecond-level speeds”. The transaction price is determined dynamically based on advertisers’ campaign goals.

Revenue recognition for AppLovin works as follows:

- Action-based: Revenue is recognized when a specified action (click, install, etc.) occurs (AppLovin earns revenue based on value delivered - advertisers typically set a target return on ad spend - ROAS - or cost per acquisition, and AppLovin optimizes bids so that campaigns hit those targets).

- Impression-based: Revenue is recognized when an ad impression is delivered.

- Adjust subscriptions: for its Adjust measurement platform (more on this below) revenue is recognized ratably over the subscription period (up to 12 months).

Advertisers pay AppLovin the agreed price; the company in turn pays the Publishers. AppLovin’s economics come from the spread between what advertisers are willing to pay and what publishers are paid in the auction. The more AppLovin is able to maximize price paid by Advertisers and minimize the price recognised to the Publishers, the higher the slice of the transaction value it keeps.

The Product

AppLovin’s advertising solutions include four core tools:

- Axon Ads Manager: The flagship AI-powered advertising product. Advertisers set user acquisition goals, and Axon’s recommendation engine (Axon AI) dynamically allocates spend across publisher inventory to optimize return on ad spend (ROAS). This product drives the vast majority of revenue.

- MAX: An in-app mediation platform that allows publishers (app developers/ gaming companies) to maximize ad revenue by running real-time bidding auctions across multiple ad networks. Revenue is generated as a percentage of client spend through the platform.

- Adjust: A mobile measurement and analytics platform offering attribution, fraud prevention, and campaign performance insights. Revenue comes from annual software subscription fees.

- Wurl: A connected TV (CTV) platform for content distribution and monetization, with revenue typically on a usage-based/CPM model.

AppLovin offers the above as an integrated suite: advertisers use Axon to acquire users; publishers use MAX to monetize inventory; Adjust and Wurl sit around that core.

How Does it Work

First of all, we need to start from how the mobile gaming advertising market works, to understand how AppLovin acts as a key infrastructure layer.

In gaming, there are three distinct monetization models — paid, ad-supported, and hybrid.

The Three App Monetization Models

Think of it like a TV analogy:

- Paid = buying a DVD (or buying a movie online, for the younger generation) (you pay once, no ads).

- Ad-supported = free broadcast TV (you watch for free, ads pay the bill).

- Hybrid = a streaming service with both a free ad tier and a premium paid tier.

In the online world, it works like this:

Model | How the user pays | How the developer earns | Examples |

Paid | Upfront purchase price | App store sale | Premium games, productivity apps |

Ad-Supported | Nothing (free download) | Advertisers pay to show ads to users | Casual games, news apps |

Hybrid | Optional: in-app purchases + optional ad removal | Ads + in-app purchases (IAP) | Most modern mobile games |

AppLovin's solution is targeted toward ad-supported and hybrid models, and it works best in the hybrid model where most modern mobile games are found today.

Axon AI and Axon Ads Manager

On the Advertisers' side, Axon AI is AppLovin’s central recommendation and bidding engine. Advertisers use Axon Ads Manager (self-serve or managed) to set campaign goals: target ROAS, CPA, budget, geography, platform, etc.

Mechanically, it works like this:

- The advertiser defines goals (e.g., “I want at least 3x ROAS at this bid cap”).

- Axon AI’s models score potential impressions using device/network information, prior engagement with apps and ads, and (if provided) advertisers’ own first‑party data.

- Based on that score, Axon computes the expected value of showing an ad to that user and generates a bid that should achieve the advertiser’s ROAS or CPA target.

- An auction takes place (via MAX or external exchanges); if Axon wins the auction, the user converts.

- That conversion (and its value) and data from those auctions feeds back into Axon.

AppLovin emphasizes that Axon is continuously self‑learning: more impressions and more conversions generate more training data, which is used to refine models in an ongoing loop. Management also states that Axon doesn’t ingest “sensitive personal information” or other bidders’ data, and that data about children’s apps is explicitly excluded.

This structure makes Axon function as a black-box performance system where the advertiser inputs goals and budgets and the system decides where, when, and how much to bid.

MAX and the ad marketplace mechanics

MAX is the in‑app bidding and mediation layer that turns publisher inventory into a high‑density auction marketplace.

Key mechanics of MAX’s auction:

- MAX operates a unified first‑price auction: the highest bid wins, and all bidders have equal access to each impression opportunity.

- When a user opens an app and a slot becomes available, MAX:

- Requests bids from bidders.

- Passes identity tokens and context in the bid request.

- Collects bids within a defined timeout (tmax).

- MAX merges these bids with legacy waterfall sources (a technical term; think of it as a network used to fill ad inventory impressions which Publishers make available to Advertisers) and selects the highest CPM bid, then notifies the winning bidder.

- After the ad loads and shows, MAX sends win or loss notifications to participants, which AppLovin explicitly notes are used as training signals in Axon’s models.

So, structurally:

- Supply side: App developers integrate MAX to maximize their revenue per impression by creating competition for each slot.

- Demand side: Axon (and other DSPs — other systems used by Advertisers to bid for ad slots) bids into those auctions, using AI to decide what each impression is worth given advertisers’ goals.

This creates a two-sided marketplace where AppLovin sits at the center, earning economics from the margin it can generate by:

- Improving targeting (better ROAS for advertisers).

- Increasing bid density and yield (better monetization for publishers).

The data & performance flywheel

The business model is designed as a data flywheel:

- More advertisers and campaigns → more impressions and conversions.

- More impressions/conversions → more training data for Axon (device/network data, engagement, win/loss signals from MAX, optional advertiser data).

- Better models → higher predicted value for good impressions, better bids, improved ROAS.

- Better ROAS → advertisers raise budgets, new advertisers onboard, and publishers see higher yields, attracting more supply.

This flywheel is visible in the economics: high gross margin and rising revenue per install.

Key Financials

Prior to the Apps divestiture, AppLovin had two segments. The table below shows the transition:

Revenue Stream | FY2022 | FY2023 | FY2024 | FY2025 (Advertising only) |

Advertising Revenue | $1,049M | $1,842M | $3,224M | $5,481M |

Apps Revenue (IAP + IAA) | $1,768M | $1,441M | $1,485M | Divested (discontinued) |

Total Revenue | $2,817M | $3,283M | $4,709M | $5,481M |

By geography:

Geography | FY2023 | FY2024 | FY2025 |

United States | $1,971M (60%) | $2,689M (57%) | $2,827M (52%) |

Rest of World | $1,312M (40%) | $2,020M (43%) | $2,653M (48%) |

The international share is expanding rapidly. In Q1 2026, Rest of World revenue was already $935M vs. $907M for the US — a near-perfect 50/50 split.

Margin evolution (Advertising segment only, continuing operations):

Year | Revenue | Adj. EBITDA | Adj. EBITDA Margin |

2023 | $1,842M | $1,236M | 67.1% |

2024 | $3,224M | $2,412M | 74.8% |

2025 | $5,481M | $4,512M | 82.3% |

Q1 2026 | $1,842M | $1,557M | 85% |

The dramatic margin expansion reflects the near-zero marginal cost of additional ad placements once infrastructure is in place: incremental revenue flows almost entirely to the bottom line. The primary cost drivers are datacenter/cloud computing costs ($543M in FY2025) and personnel costs ($207M in FY2025).

Metric | 2023 | 2024 | 2025 |

Diluted EPS | 0.98 | 4.53 | 9.75 |

Net Debt | 3,111.0 | 2,812.0 | 1,025.9 |

Return on Invested Capital | 14.3% | 39.7% | 65.3% |

Free Cash Flow | 581.1 | 2,179.0 | 4,350.5 |

The growth in EPS and FCF has been dramatic. ROIC also expanded exponentially and Net Debt has contracted to a very healthy level.

Clients

Historically, AppLovin’s core client base has consisted mostly of mobile game studios.

Since late 2024, the company has started a push to expand outside of those categories, when it opened the door to consumer advertisers, today mostly belonging to the e-commerce space.

In Q1 2026, management started defining these new categories as the “consumer vertical” and beginning in 2026 it will start expanding into other transactional categories like fintech, insurance, and lead gen.

We have no firm numbers on how much e-commerce is already contributing to revenues (it is not shown in the reported segment as a separate line) but management said that in late 2025 the contribution started to be quite meaningful and is growing faster than gaming.

As we'll see later on when we speak about potential growth opportunities, expanding into new verticals clearly represent one of the key bullish points for AppLovin.

Industry

The in-app advertising market was valued at approximately $185 billion in 2025 and is projected to grow to over $650 billion by 2035 at a ~12% CAGR, driven by several structural forces:

- Sustained growth in global mobile device penetration and time-on-app, expanding addressable inventory.

- Shift of advertiser budgets from linear TV and open web to measurable, performance-based mobile formats.

- Expansion into new verticals (e-commerce, social, fintech) beyond gaming, which AppLovin itself is pursuing, as we already discussed.

- Global app marketing spend reached $109 billion in 2025, with user acquisition ($78B) and remarketing ($31B) both posting strong growth.

- Rapid expansion of CTV as an adjacent channel, where AppLovin's Wurl platform is positioned.

Key Industry Risks

- Revenue is cyclical and correlated with macro spending: during downturns, advertisers quickly reduce budgets.

- The ecosystem is dependent on Apple and Google's app distribution duopolies, which control inventory access, payment processing, and data signals.

- The free-to-play mobile gaming segment — AppLovin's core supply base — faces user engagement saturation in mature markets.

- Advertiser concentration risk: reliance on a limited set of large gaming studio spenders means any pullback is amplified.

Competition

It is not easy to define who are AppLovin's main competitors, because AppLovin offers an integrated suite made up of different pieces that go together and each has a different subset of competitors by itself.

In general, the most direct competitors are Unity/ironSource, Google AdMob, Liftoff, Moloco, Mintegral, and a smaller set of mediation / monetization specialists such as Appodeal. None of them though reach the scale and the performance of AppLovin.

AppLovin’s own business has become more focused after the June 2025 sale of its Apps business; its remaining platform is a single reportable segment built around Axon Advertising, MAX, Adjust, and Wurl. That makes it more of a pure-play ad-tech and AI-driven performance marketing company than before, which further restricts competition (many competitors also are present in other niches or businesses).

Competitive position

AppLovin’s competitive position appears very strong in mobile performance advertising and app monetization. Management says the company sits at the nexus of the ad ecosystem, reaches roughly 1.4 billion users per day, and benefits from a self-reinforcing data flywheel that improves its AXON engine as scale grows.

The clearest evidence of strength is margin expansion and business concentration after the Apps divestiture: 2024 revenue was $4.709 billion with net income of $1.580 billion, and the 2025 platform-only model shows even higher profitability. AppLovin also says it believes it competes favorably on technology, ecosystem knowledge, user reach, third-party relationships, and its ability to execute strategic transactions.

AppLovin looks like a scaled winner in a concentrated, winner-take-most segment, with (so far) limited competition from various companies which operate in the more general online advertising space.

The company’s real advantage is not that competitors are absent; it is that its AI-driven optimization, publisher relationships, and data scale currently seem strong enough to keep winning share despite those competitors.

The Moat

AppLovin appears to have a real moat, but it is not a classic consumer-brand moat. It is mainly a combination of data/network effects, switching costs, and scale-driven process advantages, with some intellectual-property and brand support around the edges.

The strongest moat looks like a data-driven network effect moat. As more advertisers use its solutions, it gains more user and engagement data, which then strengthens Axon AI and improves matching, targeting, and monetization performance; that creates a self-reinforcing loop between usage, data, and product quality.

Why we think it is durable

There are a few reasons this could persist:

- Data accumulation advantage. The company explicitly says its data improves Axon AI, and that better model performance improves the effectiveness of its advertising solutions.

- Scale and speed. Axon Ads Manager runs auctions at “vast scale” and “microsecond-level speeds,” which suggests operational scale is part of the advantage.

- Workflow embedding and switching costs. Advertisers use AppLovin for campaign management, optimization, measurement, and reporting, which can make the platform sticky once integrated into marketing workflows.

- Cross-product ecosystem. MAX, Adjust, Wurl, and Axon Ads Manager give the company multiple entry points.

What kind of moat it is not

It does not look like a strong monopoly-style moat or a pure regulatory moat. Management repeatedly emphasizes that the market is fragmented and competitive, and it also warns that third-party platforms can change rules in ways that hurt the business (more on this later). That means the moat is very powerful but not completely impenetrable.

Stock Price & Performance

As of June 2, 2026, AppLovin trades at around $600 per share (from an all time high of around 745 dollars, in September 2025), with a market cap of around $203 billion. Price total return is +50% over 1 year, +2,341% over 3 years, and +764% over 5 years.

In the last year, the stock has been under pressure for a number of significant reasons:

Short-Seller Allegations

A number of well-known of investment firms specialized in short selling have made several allegations against AppLovin. The core themes are: ad fraud / deceptive ad practices, misuse of platform data, and money-laundering / illicit-funds claims.

Let's go into the details.

- Ad fraud and deceptive advertising

One set of short reports, starting in February 2025, alleged that AppLovin’s rapid growth was driven by “advertising fraud” and low-quality ad inventory. These reports claimed the ads were deceptive, predatory, or hard to click, and that the company’s revenue growth was not as clean as it appeared.

- Data theft / platform policy violations

Another major allegation was that AppLovin reverse engineered or extracted proprietary data from other platforms, especially Meta and other app ecosystems, to improve its ad targeting. Short sellers also claimed AppLovin violated app-store terms, used “fingerprinting,” and relied on tactics like “silent install” or “backdoor installation” schemes to inflate app downloads or target users without proper consent.

- Money-laundering / illicit capital claims

A 2026 CapitalWatch report went further and alleged that AppLovin was a “digital laundromat” or “safe haven” for illicit funds tied to Chinese and Cambodian criminal networks. That report suggested the company’s AXON algorithm and “Silent Install” mechanisms could be used to convert “black money” into legitimate ad revenue, and it also raised accusations about the sources of some shareholder capital.

- SEC Probe

In addition to the allegations above (and on the back of those), AppLovin is also under a SEC investigation over its data-collection and ad-targeting practices. The probe reportedly centers on whether the company violated platform partners’ service agreements and used unauthorized tracking methods, including fingerprinting-like techniques, to deliver more precisely targeted ads.

The case first surfaced in October 2025 and remains active and ongoing. As of today, the SEC has not publicly accused AppLovin of wrongdoing, and no enforcement action or settlement has been announced so far.

Are These Allegations Credible and What Could Happen

Of course we do not know if these allegations are true; what we know is that, so far, no action has been taken against the company (but the stock suffered a significant drop from all-time highs).

In our view the allegation that might have at least some credibility is the claim that AppLovin may have engaged in aggressive data-collection or targeting practices that could conflict with platform rules or attract regulatory scrutiny; less credible, or at least much less substantiated publicly, are the more extreme claims about systematic fraud, “digital laundering,” or broad criminal links.

AppLovin of course has publicly denied these accusations and pushed back forcefully but the SEC probe gives the platform/data allegations more weight, because it suggests regulators found enough in the short-seller reports to at least look into whether AppLovin violated partner agreements or used unauthorized tracking methods such as fingerprinting.

If found guilty, the biggest risks are:

- Regulatory enforcement. The SEC could pursue sanctions or require changes if it finds AppLovin violated partner agreements or privacy-related rules.

- Platform retaliation. Apple, Google, or Meta could limit AppLovin’s ability to use certain tracking pixels or data methods, which would weaken ad targeting and make it harder to win advertisers.

- Fines and legal costs. Even if the monetary penalty is manageable relative to cash flow, defense costs, settlements, and follow-on litigation could still be meaningful.

- Loss of trust. Advertisers, publishers, and partners may become more cautious, especially if the issue is framed as opaque tracking or policy evasion.

- Business-model damage. If the tracking method is part of the core performance engine, AppLovin may need to redesign products, which could reduce targeting precision and performance.

If the unauthorized-tracking allegations are true, the biggest risk is not just a fine — it is that major platform partners could restrict, suspend, or condition AppLovin’s access to their ecosystems, which could directly hurt growth. The most serious outcome would be a forced reduction in data access or tracking capability, because that could impair Axon’s effectiveness and hit growth at the source. A fine alone is annoying; a change in platform access could actually damage the moat.

Our Take

On paper, AppLovin is one-of-a-kind company, a rare combination of very fast growth, very high margin, and extraordinary cash conversion, all characteristics of great compounders and high-quality companies, exactly what we are looking for here at The Quality Investor Letter.

The company operates in the online advertising industry, which by definition is already a high margin / low capital intensity (high ROIC) sector (think Google, Meta, etc.). What is even more interesting, is that AppLovin presides the mobile gaming ad segment, through an AI-driven ad platform that seems to get stronger as more advertisers use it, with a clear and widening network effect moat.

Applovin’s main bull case is indeed that it is building a self-reinforcing advertising engine: more advertiser usage brings more data, which improves Axon AI, which improves ad performance, which attracts more advertisers and monetization partners. If that loop keeps compounding, the business can widen its performance gap over smaller competitors.

The business is still growing at a very high rate even at scale. Revenue increased from $1.84 billion in 2023 to $3.22 billion in 2024 and $5.48 billion in 2025, while adjusted EBITDA rose from $1.24 billion to $2.41 billion to $4.51 billion over the same period. That kind of combination—top-line growth plus margin expansion—is exactly what long-duration compounders tend to look like in their best years.

The bull argument is strengthened by AppLovin’s remarkable profitability. Adjusted EBITDA margin expanded from 67.1% in 2023 to 74.8% in 2024 and 82.3% in 2025, while net margin reached 60.8% in 2025. That tells you the company is not just growing; it is also converting a very large share of incremental revenue into earnings and cash.

Free cash flow is one of the strongest parts of the bull case. AppLovin reported free cash flow of $1.04 billion in 2023, $2.07 billion in 2024, and $3.95 billion in 2025, with 2025 free cash flow margin at roughly 72% of revenue. For equity holders, that matters because it gives the company a lot of optionality: buybacks, acquisitions, product investment, and balance-sheet flexibility.

The platform itself looks powerful because it combines ad buying, monetization, measurement, and analytics. Axon Ads Manager is the core revenue engine, MAX improves publisher monetization, Adjust provides measurement, and Wurl gives exposure to connected TV. This multi-product footprint deepens customer relationships and makes AppLovin harder to displace than a single-purpose ad tool.

Growth Runway

Gaming

AppLovin’s penetration in gaming, its core, is already very high, and growth in the future will probably not come from taking more mediation share but from the market itself expanding as more games, more impressions, and more ad supply flow through the ecosystem. Management itself has stated that gaming could still support a 20 to 30% YoY growth in the years to come. There also still room to grow in efficiency, because AppLovin states that it only converts a small portion of the impressions it serves, so better models can raise yield even without huge share gains.

But the company is no longer confined to one narrow use case. It is expanding beyond mobile gaming as it believes its technology can be applied across more verticals and content industries. What makes this expansion structurally significant is indeed that AppLovin is not building new technology from scratch; it is applying an already battle-tested, high-margin advertising recommendation engine to new demand pools, serving a base of 1 billion+ daily active users. If those adjacencies work, the market could still be underestimating the size of the runway.

New Verticals

E‑commerce / web consumer advertisers: AppLovin has an explicit “consumer” (e‑commerce/web) vertical that management says is already scaling faster than gaming and is already delivering improved ROAS for those advertisers; the platform opening (self‑serve) in June will accelerate adoption.

This is by far the most advanced and impactful new vertical. AppLovin launched a pilot program for web-based e-commerce advertisers in Q4 2024, quietly onboarding hundreds of direct-to-consumer brands. By Q1 2025, the e-commerce cohort had already reached a ~$1 billion annualized run rate, with less than 1% penetration of the total addressable advertiser market — CEO Adam Foroughi explicitly noted that Meta alone has over 10 million active advertisers, illustrating the sheer scale of the untapped opportunity.

By Q1 2026, the company had rebranded the category as the "consumer vertical" (broadening the scope beyond pure e-commerce to any business seeking performance-based customer acquisition) and reported an acceleration: the consumer vertical exited Q1 2026 with March growing roughly 25% more than January, and April 2026 set a record month in advertiser spend, surpassing any peak Q4 2025 month. The platform is going live publicly for general access under the brand Axon in June 2026, marking a watershed moment after 14 years of operating as a closed platform.

The consumer vertical's TAM is enormous. Total ad spending across all formats is projected to exceed $1.26 trillion in 2026. AppLovin's management specifically references its 1 billion+ daily users spending ~85–90% of their mobile time in non-gaming activities, arguing this makes it a compelling surface for virtually any performance advertiser — from beauty brands to insurance companies.

Connected TV (CTV): via Wurl (acquired), AppLovin targets CTV ad inventory, distribution and FAST channels—management states they are applying Axon to CTV and building products like AdPool and TVBits. This is an adjacent addressable market they are operating in today.

The biggest new market near term is self-serve access for advertisers in June, which should open the platform to many more businesses globally.

A major theme is also that Axon is becoming more automated and easier to use. AppLovin is rolling out AI creative tools, including an interactive page generator already broadly available and a video generator that is nearing full release, with the goal of letting advertisers onboard, create ads, and scale without human help. Management also emphasizes agent-compatible infrastructure, so AI agents can manage campaigns directly inside the platform.

The unifying thesis across all verticals is the data flywheel: every new advertiser category (e-commerce, lead gen, CTV) feeds richer behavioral data into Axon AI, making the gaming models smarter and vice versa. A consumer who buys a $4,000 handbag is statistically likely to be a high-value spender in a match-3 game — and Axon can discover thousands of such cross-correlations autonomously. This means expansion into new verticals is not just additive revenue; it is a structural capability enhancer that compounds the moat in every existing market AppLovin already dominates.

So, it’s all good?

Risks

The reality is that there are some risks that cannot be underestimated.

AppLovin is structurally exposed to a few things that are hard to fix:

- Dependence on third-party platforms: AppLovin is 100% dependent on the platform owners. It is like if it is renting an apartment in an upscale and luxurious building; the apartment may be magnificent, but AppLovin does not own the building. If you behave badly, or the owner simply changes some rules, this could have a disproportionate impact on your stay. Changes at Apple, Google, Meta, and similar platforms could reduce data utility and hurt ad effectiveness. If privacy changes, platform policy changes, or reduced signal quality weakens Axon AI performance, the company’s targeting and monetization effectiveness could deteriorate, which would hit both revenue growth and pricing power. And allegations against the company do not necessarily have to be true for something like this to happen. Remember when Apple made tweaks to its privacy and tracking rules and Facebook entered panic mode?

- Concentration in the mobile gaming ecosystem: AppLovin’s product exists in the mobile gaming ecosystem. And this segment is dependent on games quality, gamers behavior and other industry specific issues that can influence advertising spending. In addition, advertising in general is tied to the economic cycle: a recession or decrease in advertising spending could hit AppLovin growth rates and bottom line disproportionally. Bear in mind that the company also lacks long-term client commitments, which means revenue can move quickly if advertisers reduce spend, switch platforms, or decide competitors are better. That makes the business more cyclical and more fragile than the headline growth rate suggests.

- Growth opportunities prove less attractive than they appear to be: Another risk is that growth into e-commerce, CTV, and other adjacent markets may be slower or less profitable than management expect. Management itself says these are still expansion efforts, and the company acknowledges that new market launches can take time, may fail, or may require more capital and management attention than planned. Game ads work very well when a user is already playing another game, Nice! Click, install. But when it is a car insurance ad, will the gamer be as interested?

So, what is our conclusion?

The truth is that AppLovin’s is indeed an exceptionally high-quality company, but this very same quality is tied to external dependencies the company has very little control over.

The bull case is credible and economically powerful: AppLovin is a high-margin AI ad platform with a scalable data flywheel, and if execution remains strong, the stock can plausibly keep trading at premium multiple over time.

However, risks are also substantial, and need to be taken into consideration.

How do we solve this conundrum?

The best way is to apply a wide margin of safety, so that in case any of the risks does indeed materialize, our investment is somewhat protected.

Valuation

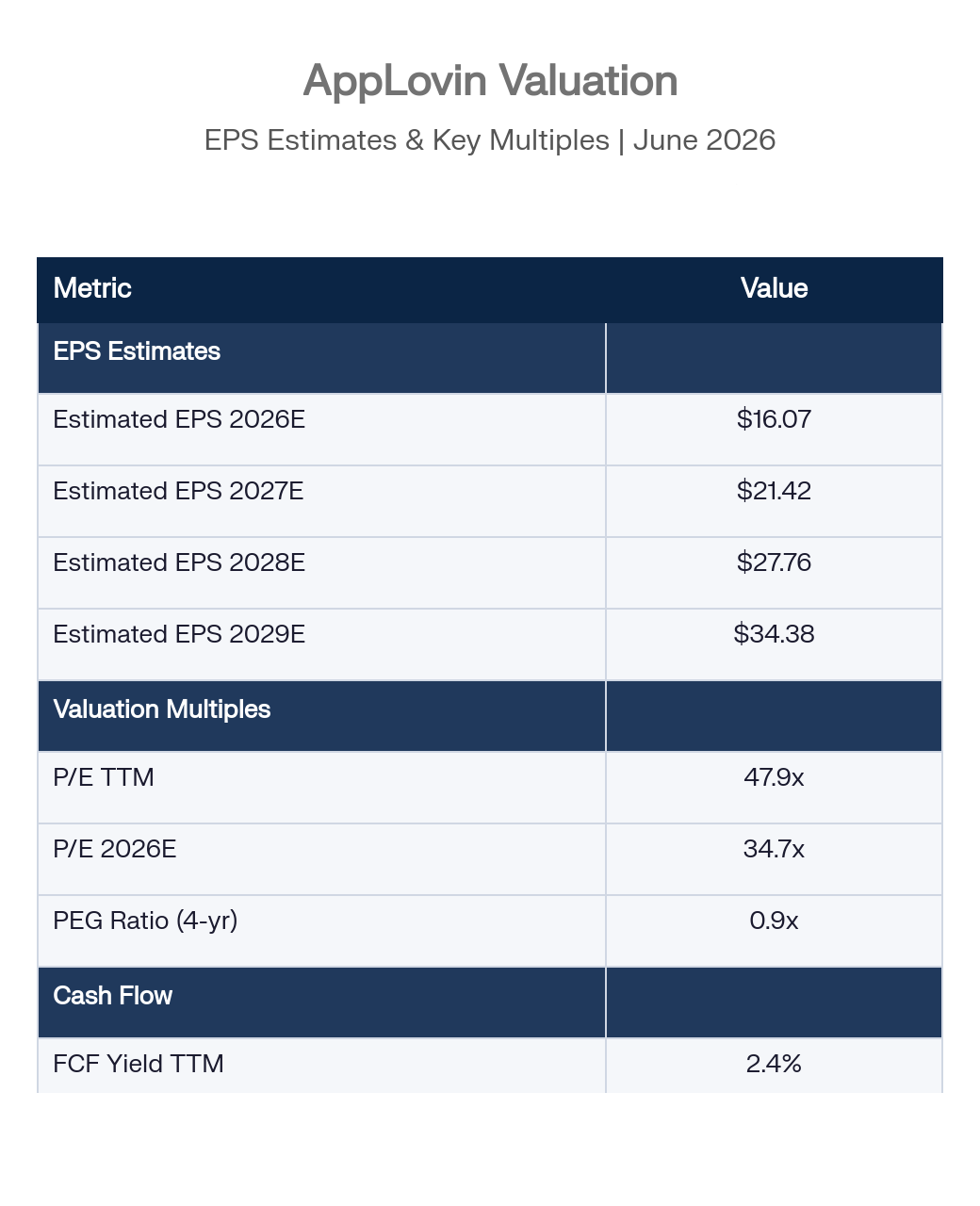

The market is currently valuing AppLovin at a P/E TTM of 47.9x and a P/E 2026E of 37.7x with PEG Ratio (4-year) of 0.9x. FCF Yield stands at 2.4%.

The market appears to view AppLovin as a high-quality, high-growth, high-margin ad-tech compounder. Valuation might seem optically high, but expected growth is also very high, so it does not seem to trade at unreasonable levels (it is probably discounting the uncertainties regarding the ongoing investigations).

If we didn’t see any risk, probably this would be a fair entry point. However, AppLovin’s current valuation leaves very little room for any slowdown, margin compression, or confidence shock. The stock can work if the company keeps compounding growth, maintains exceptional margins, and avoids regulatory or reputational damage; if any one of those breaks, the multiple might fall fast.

If we invest at these prices, the most likely way to lose money is not necessarily a collapse in revenue; it is a multiple compression event. If growth decelerates even modestly, or if any external shock materializes, the market could re-rate the stock sharply downward.

In other words, you do not need a disaster to lose money; you only need the business to be “very good” instead of “exceptional.” At this valuation, that gap matters a lot.

So, what would be a good entry point?

Intrinsic Value & Potential Returns

If we run a quick DCF, we find that AppLovin is trading at a level that implies a FCF annual growth of 20% for the next 5-years; not unreasonable (in the last three years FCF grew at an annualized rate of close to 80%!). If we push up the growth rate to 30%, the intrinsic value of $900 implies a 35% price-to-value discount.

| FCF Annual Growth | Terminal Growth | Intrinsic Value |

|---|---|---|

| 30% | 2% | $900 |

| 20% | 2% | $600 |

| 15% | 2% | $485 |

If we take current analysts' expected EPS growth rates as plausible, with a 30x P/E exit multiple in 2029, we would have an annualized return of close to 17%, if we invested at today's price. If the stock re-rates, the return would be much lower.

| Exit Multiple | 4-Year CAGR |

|---|---|

| 20x P/E | 5.4% |

| 25x P/E | 11.4% |

| 30x P/E | 16.6% |

If you have been following The Quality Investor Letter for some time, you know we look for a hurdle rate of at least 20% and a margin of safety of 30 to 50%.

At today's prices these two conditions are met only if the stock continues trading at 35-40x P/E with at least a 30% growth in earnings and free cash flow YoY. It might very well happen, but the margin of safety is near zero.

While we regard AppLovin as a potential investment candidate, we are not buyers at these levels. There are many things that can go at least a little bit wrong, and we need a good margin of safety today to protect us against these risks.

This is what we do instead: We add AppLovin to our Quality Investor Watchlist and we'll keep an eye on it and further investigate the company and its business. If the valuation pulls back to levels that provide a wide margin of safety, we will reconsider our position for a potential buy.

Member discussion